by Ken Sehested

While the nation’s eyes were recently glued to the former FBI Director James Comey’s testimony before the Senate Intelligence Committee hearings, the House of Representatives quietly passed the Financial Choice Act which rolls back much of the 2010 Frank-Dodd Wall Street Reform and Consumer Protection Act, enacted to prevent another round of reckless behavior by banks and other major financial institutions that created the Great Recession of 2007.

§ § §

“For scoundrels are found among my people; they take over the goods of others. Like fowlers they set a trap; they catch human beings. Like a cage full of birds, their houses are full of treachery; therefore they have become great and rich, they have grown fat and sleek. They know no limits in deeds of wickedness; they do  not judge with justice the cause of the orphan . . . and they do not defend the rights of the needy.” —Jeremiah 5:26-28

not judge with justice the cause of the orphan . . . and they do not defend the rights of the needy.” —Jeremiah 5:26-28

§ § §

More on the Financial Choice Act below, but first . . .

I nearly cried this afternoon, pushing my old mower to the curb, with a “FREE” sign taped to the handle. I was happy that by the time lunch was finished, someone had already swept it up in their arms. (That’s the way I image it.) At least a few parts may live on. I’m not positive of its age, but at least 23 mowing seasons—every year, until last, firing up on the first pull of the spring. Duct tape secured the gas tank; the carriage had a serious crack; tread completely worn off the wobbly wheels; metal so corroded that I had to use a putty knife to scour its underbelly of sweet-breathed layers of grassy-weed residue after each mow.

I like old things, and not just because I’m on Medicare’s tab. I still remember my first pair of “Sunday” shoes, the stiff-leather kind that takes hours of wear before they no longer torture your feet. And since I only wore them on Sundays, that took months.

Having steered all my autos to their last lap, I regretted every parting, and still remember each by their assigned nickname. I buried a favorite pair of hiking boots in the high desert surrounding Ghost Ranch in New Mexico—they were already limped and came completely undone before week’s end. I could not bear to lay them in the trash as so much litter.

It’s an odd habit, I know, to treat mere stuff with such affection. But I’m not embarrassed in doing so. My 22-year-old Roper boots have cracks, but still shine up like a fine mirror.

§ § §

The US has the 4th highest degree of wealth inequality, behind Russia, Ukraine, and Lebanon.[1]

§ § §

“Let’s cut to the chase,” Sen. Al Franken said in a statement this week about the House of Representatives’ stealth approval (by partisan majority, a lone Republican voted nay) of the Financial Choice Act. “This is a straight out giveaway to Wall Street bigwigs, bankers, and firms, who are salivating over the  opportunity to once again gamble with hard-working Americans' money without fear of repercussion.”[2]

opportunity to once again gamble with hard-working Americans' money without fear of repercussion.”[2]

Ever wonder why no one in Congress ever speaks up on behalf of easy-earned money? Me neither. But that’s what this bill is about.

The majority of citizens still feel the pinch of the financial meltdown that began in 2007; but the dip was short-lived for a few. The nation’s biggest banks hit new profit levels in 2016, the third such records in the last four years.[3]

Over the course of the Great Recession, nearly $13 trillion[4] disappeared.[5] Eight million lost their jobs. Nearly four million homes were foreclosed. Median household wealth fell 35%. Two-and-a-half million businesses went under. Income inequality reached its widest margin since the Great Depression of 1929, with 95% of the economic recovery since then going to 1% of earners.[6]

Can you guess how many captains of finance were convicted of maybe of the largest thefts in history? That would be 00,000,000,000,000.00. Shoplifters fare worse.

In a 2006 speech to academic economists, Berkshire Hathaway holding company partner Charlie Munger rhetorically asked “Is there a functional equivalent to embezzlement?”, commenting on the all-too-common habits of investment firms and financial advisors who take risks that would shock horse race bookies.[7] “You can see why I don’t get invited to many lectures,” he admitted.

§ § §

“We can have democracy in this country or we can have great wealth in a few hands, but we can not have both.” —former US Supreme Court Justice Louis Brandeis

§ § §

After the Wall Street frenzy unraveled the nation’s (and, nearly, the globe’s) economy, Congress  approved a bundle of new regulations known in abbreviated form as the Dodd-Frank bill, meant to forestall financial institutions from gambling with the public’s money. The Financial Choice Act,[8] if approved by the Senate, would remove most of the Dodd-Frank bridle from the scavengers’ mouths.

approved a bundle of new regulations known in abbreviated form as the Dodd-Frank bill, meant to forestall financial institutions from gambling with the public’s money. The Financial Choice Act,[8] if approved by the Senate, would remove most of the Dodd-Frank bridle from the scavengers’ mouths.

Of particular significance, the work of the Consumer Finance Protection Bureau (CFPB) would be threatened—if not its existence, at least its independence. That’s the agency that receives, on average, 25,000 complaints each month about banks, credit card issuers, mortgage lends, student loan servicers and other financial productions’ fraudulent practices. Since the end of the Great Recession, the CFPB has returned nearly $12 billion to an estimated 29 million consumers defrauded by financial institutions.[9]

You don’t need a long memory to recognize the CFPB’s value. Remember the Wells Fargo Bank scam brought to light in 2016, when over the course of five years the bank’s employees “created more than 1.5 million sham checking accounts and applied for 565,000 credit cards, using customer names and money. Customers were charged unnecessary fees, saw their credit scores fall or were simply confused when debit and credit cards they never asked for showed up in the mail.” In fact, as early as 2002 the company’s own internal auditor reported a spike in what they called “sales integrity” cases. The system gaming was truly systematic and longstanding, not the sudden onset of an evil design by a few rogue operatives.[10] The deceit was in the blood.

Wells Fargo was fined $185 million, the largest such penalty in banking history. But given the bank’s 2015 profit of $22.9 billion, the fine was more of a nuisance than a penance.

The year before the Wells Fargo disclosure, the CFPB caught Citibank defrauding its credit card customers by charging for benefits they didn’t receive. There’s much more, but enough for now.

A January survey by Consumer Reports revealed that two-thirds of respondents doubt that banks and other financial institutions can be trusted.[11] Not for no reason: The House’s new bill would roll back the  “fiduciary rule” which requires financial advisors to act in the best interests of their clients(!), as opposed to steering said clients to investment plans that create larger fees for brokers and advisors.

“fiduciary rule” which requires financial advisors to act in the best interests of their clients(!), as opposed to steering said clients to investment plans that create larger fees for brokers and advisors.

Thankfully, the Financial Choice Act will likely be reconfigured in the Senate, much as will the House’s American Health Care Act. But don’t get your hopes up, for we are in a political and financial climate that upholds the rule of gold: If you can get it, you should get it—and you deserve getting it. It’s not a con if you don't get caught.

§ § §

"Now as through this world I ramble / I see lots of funny men / Some rob you with a six gun / And some with a fountain pen." —Woody Guthrie lyrics in "Pretty Boy Floyd"

§ § §

Just as Trump is not responsible for, but is reflective of, our current political maelstrom, the financial debauchery of recent years is not an overnight phenomenon. It’s been there from our beginning, at least as fall back as John Locke’s considerable influence on our founding culture.

In the words of political philosopher C.B. Macpherson’s seminal book, The Political Theory of Possessive Individualism: Hobbes to Locke, it was Locke, the 17th century philosopher, who asserted “the individual right of appropriation overrides any moral claims of the society. . . . [Locke] has erased the moral disability with which unlimited appropriation had hitherto been handicapped,” justifying “as natural, a class differential in rights and in rationality, and by doing so provides a positive moral basis for capitalist society.”[12]

Locke’s was a “prosperity gospel” before the phrase was coined, and it was embedded not in divine right but, secularly, in the nature of reality itself. He can be said to be modernity’s most brilliant defender of Mammon and a society’s political economy stripped of all transcending bounds and covenant bonds. Wealth, in his vision, is simply bracketed from moral interrogation. And Mammon’s modern spelling in Market.

Not even Adam Smith, the 18th century philosopher considered the founder of classical free market economics, shared Locke’s optimism of human rationality. He knew that “free” markets could be dominated by a small class of financial vigilantes and required a larger regulatory climate—social, moral, as well as legal—to stem the rule of gold, writing

“The proposal of any new law or regulation of commerce which comes from merchants and manufacturers should always be listened to with great precaution, and ought never to be adopted till after having been long and carefully examined with the most suspicious attention."[13]

I never cease to be amazed, throughout my entire career as an itinerant preacher and organizer within the faith community, at how few people recognize that our nation’s political aspirations are often in conflict with our economic interests. It was Jesus—millennia before Karl Marx posited the primacy of economics in  human behavior—who said that “where your treasure is, there will your heart be also” (Matthew 6:21).

human behavior—who said that “where your treasure is, there will your heart be also” (Matthew 6:21).

§ § §

“Whoever has the power to alleviate this evil, but deliberately opts for profit by it, should be condemned as a murderer.” —Basil of Caesarea, 4th century bishop in Cappadocia (in modern-day Turkey), speaking of wealthy landowners who hoard their stockpiles of grain, then sell at inflated prices during a famine

§ § §

“We do not believe that the God we know will have to do with things,” theologian James McClendon wrote in the first volume of his Systemic Theology.[14] “Yet this biblical materialism is the very fiber of which the first strand of Christian ethics is formed.”

More plainly spoken: God loves stuff.

Do you remember the advice Screwtape gave to Wormwood in C.S. Lewis' devotional classic, Screwtape Letters? In discussing the case of one particular human that Wormwood is attempting to subvert, Screwtape—the Satan-like central character of the book—offers this bit of advice to Wormwood, his disciple:

"It is, no doubt, impossible to prevent his praying for his mother, but we have means of rendering the prayers innocuous. Make sure that they are always very 'spiritual,' that he is always concerned with the state of her soul and never with her rheumatism."

In Scripture, “spiritual” reality is not segregated from “material” reality. Rather, spiritual reality is the descriptive account of the ordering of the material. “Righteousness” and “justice” are organically connected, in the same way that “wickedness” and “injustice” are twins. God breaks the bows of the mighty and lifts the poor from the dust was at the core of Hannah’s hallelujah (1 Samuel 2); and in similar fashion, Mary’s hymn of spiritual praise entails the dethronement of the mighty and feasts for the hungry (Luke 1).

God, we are shocked to learn, takes sides. In the evocative words of Clarence Jordan, “God is not in heaven and all's well on the earth. God is on this earth and all hell's broke loose!”

The ordering of earth’s wealth is reflective of earth’s health. Hell breaks loose whenever embezzlement breaks out. Or as the Zimbabwean proverb puts it, “When there is something wrong in the forest, there is something wrong in society.”

No topic in the Bible gets more persistent (not to mention inflamed) attention than the pattern and structure and framework of equitable sharing of the earth’s bounty—which is itself not merely the happenstance of Creation but the very countenance of God’s presence among us.

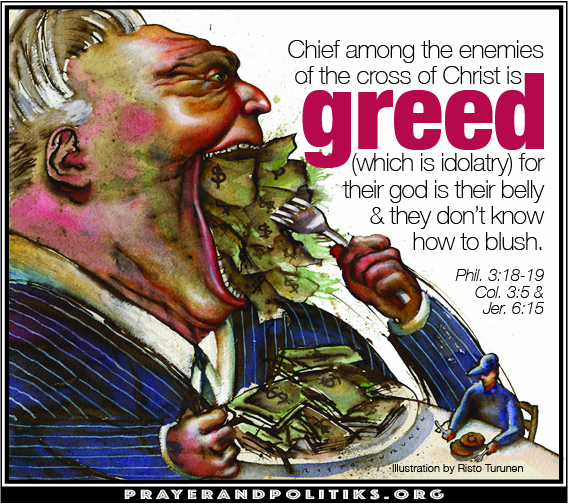

When you stick it to your neighbor, you’re sticking it to the Abba of Jesus. When you shorten the breath of those on the margin, you are simultaneously constricting the Breath of the Spirit in your own lungs. In vivid Pauline language, greed is synonymous with idolatry (Colossians 3:5); when your belly (e.g., your desires, your security demands) becomes your god, you are the “enemy of the cross” (Philippians 3:18-19). I can assure you, those texts are never read in White House prayer breakfasts.

§ § §

“Steal goods and you’ll go to prison, steal lands and you are a king.” —Japanese proverb

§ § §

Among the urgent callings of the church—arguably, the most important—is to undermine the moral legitimacy of gangster capitalism; to reaffirm the Golden Rule’s primacy over the rule of gold; to mock what my  friend Andy Loving calls "the god of fiduciary responsibility" (maximization of profit without reference to any other values). What is urgently needed is clarifying what’s at stake—that such matters are not just “politics” but questions of apostasy versus covenant faithfulness.

friend Andy Loving calls "the god of fiduciary responsibility" (maximization of profit without reference to any other values). What is urgently needed is clarifying what’s at stake—that such matters are not just “politics” but questions of apostasy versus covenant faithfulness.

I dare say this is at the heart of worship, for worship is the context of deciding worth. More than proper ritual etiquette and pious declaration, worship involves the discernment of whose promises and purposes are trustworthy. Who, finally, holds the future, regardless of current evidence? On whose provision dare we bet our assets.

I wish I could say there are reasons for optimism in our current climate. But, alas, we are immersed in a political tradition that mocks Scripture’s insistent warning: “Do not say to yourself, ‘My power and the might of my own hand have gotten me this wealth’” (Deuteronomy 8:17). To proclaim "America first" is not only diplomatic folly and a threat to democratic legacy. It is heresy.

Pessimism, however, is no reason to abandon hope. “Thing are not getting worse,” counsels the poet adrienne maree brown. “Things are getting uncovered.” Hard times draw us onto fertile ground whereby visionary insurrection is birthed. The One whom we adore has a marked ability to roll away the tomb’s seal, even those within the empire’s cemetery.

Stuff matters. This is the meaning of the Incarnation, our most unique theological affirmation. The Spirit traffics in human affairs. If God is more taken with the agony of the earth than with the ecstasy of heaven, so then should we.

# # #

©ken sehested @ prayerandpolitiks.org

Endnotes

[1] http://inequalityforall.com/fact-4/

[2] https://www.franken.senate.gov/?p=press_release&id=3717

[3] http://money.cnn.com/2017/03/03/investing/bank-profits-record-high-dodd-frank/index.html

[4] Having a hard time imaging a trillion of anything? Maybe this will help: A million seconds is 12 days. A billion seconds is not quite 32 years. A trillion seconds is 31,688 years.

[5] https://www.corporatecrimereporter.com/news/200/costofwallstreetcollapse09122012/

[6] http://www.ipr.northwestern.edu/about/news/2014/IPR-research-Great-Recession-unemployment-foreclosures-safety-net-fertility-public-opinion.html

[7] http://www.businesspundit.com/we-make-money-the-old-fashioned-way-confidence-work/

[8] “Choice” being one synonym of “freedom,” as in “everyone is free to check in to Trump Hotel in New York city.” Whenever “freedom” is mentioned, the discerning listener should always ask “free for whom?”

[9] http://www.cbsnews.com/news/gop-assault-on-consumer-financial-protection-bureau-may-succeed/

[10] http://www.businessinsider.com/cutthroat-sales-culture-wells-fargo-vanity-fair-2017-5

[11] http://www.consumerreports.org/consumer-financial-protection-bureau/why-consumer-financial-protection-bureau-is-in-danger/

[12] Quoted in Walter Brueggemann, Money and Possessions in the Bible. Westminster John Knox, 2016, p. 210.

[13] The Wealth of Nations: Book IV Chapter VIII, p. 145, paras. c29-30.

[14] James William McClendon Jr., Ethics, Nashville, Abingdon Press, 1986, p.91